US stocks reach all-time high as government shuts down

George Orwell is reported to have remarked famously that telling the truth would be a revolutionary at a time of universal deceit. It cannot be more apt than now when financial markets are dancing to the commentary that is peddled by central banks and other cheerleaders that the world is embarking on a self-sustaining recovery even as the IMF and the World Bank are reducing their growth forecasts. The United States emerged from a fortnight long government shutdown in October. The US Congress voted to lift the debt ceiling but for three months. GDP growth in the fourth quarter in the United States will be lower than previously estimated. The Bloomberg Consumer Comfort Index at minus 37.9 is at its worst level since October 2012. It has fallen for six weeks in a row.

Some indicators in Europe are turning up but it is not yet clear if Europe has what it takes to achieve a self-sustaining recovery. Export growth in Asia – China, Taiwan and Korea –slipped in September. Although October foreign trade data improved in China, it is hard to see a sound economic rationale for the rebound to sustain. No one is prepared to tell financial markets and investors that rising asset prices without fundamental improvement simply means that they are blowing bubbles. US banks have, almost uniformly, reported disappointing results. The few that did report better results have resorted to the use of clawing back loan-loss reserves to shore up profits. IBM has reported its sixth straight quarter of declining revenues. Corporate profits were flat in the US in 2012. Yet, Earnings per Share (EPS) of S&P 500 companies went up slightly in 2012 only because companies bought back shares. The rise in the S&P 500 index stock value is entirely due to an expansion of P/E multiple. To put it bluntly, that is bubble blowing, especially when fundamental economic and corporate backdrop are both turning unfavourable.

The final denouement of this bubble-blowing behaviour is the price of the stock, Twitter (TWTR is the stock code). It opened for trading at USD26.0 on 7 November and jumped to an intra-day high of USD50.09 before closing at USD44.90. That is a one day jump of 72.7%. According to John Mauldin’s research note (‘Bubbles, bubbles everywhere’, Nov. 2, 2013), “since 1990, the P/E multiple of the S&P 500 has appreciated by about 2% a year; in 2013, the S&P's P/E has increased by 18%!” He was citing another market commentator Doug Kass. Some of the worst debt practices of the 2007-08 period are back.

It is hard to believe but true that barely after five years of the last crisis of such a huge magnitude, policymakers and investors are blowing big bubbles again. Investors are obsessed with the liquidity provision by central banks. Mohamed El-Erian of PIMCO has brought out this point rather well in a recent commentary:

In normal (healthier) times, markets look to central banks to provide the appropriate regulatory and monetary policy environment; and central banks look to markets to deliver efficient pricing and resource allocation. Today, this co-dependence has become a lot less healthy.

Markets are now conditioned to expect a solid and continuous “central bank put”; and the revealed-preference of central banks for repeated interventions to support asset prices undermines efficient market functioning and discipline. For their part, and as illustrated as recently as last month’s non-decision on tapering by the Federal Reserve, central banks find it hard to reduce their direct market interventions lest they cause severe disruptions to market pricing, liquidity and financial conditions – as indeed occurred after the May 22 mention of “taper” by Fed officials.

Source: http://blogs.ft.com/the-a-list/2013/10/15/the-artificial-fuel-for-growth-cannot-last-forever

On October 30, the US House of Representatives passed, with bipartisan support, legislation “that would roll back a major element of the 2010 law intended to strengthen the nation’s financial regulations by allowing big banks like Citigroup and JPMorgan Chase to continue to handle most types of derivatives trades in house”. (http://dealbook.nytimes.com/2013/10/30/house-passes-bill-on-derivatives/). The interesting part is that Citigroup lobbyists wrote about 70 of the 85 lines of the House Bill. With this, the House has passed eight bills this year that would roll back provisions of Dodd-Frank.

Now, in any other country, it would be a major scandal if the regulated wrote the law that would regulate them. It is one thing for lawmakers to seek their views before a law is amended or passed. It is another thing to let them write the provisions that they would like to see. It has ‘Conflict of interest’ written all over it. Unfortunately, America remains the intellectual leader for global financial capitalism. Practices such as these, in combination with reckless monetary policy and investors’ carefree attitude, makes America a big risk to international financial stability.

China Credit Taps running again

Turning to China, even as analysts wrote copiously on the Fitch downgrade threat to US sovereign debt, they completely ignored the press release that Fitchratings put out on the same day. Fitch had tied China’s ratings to economic rebalancing. Of course, Fitch appears to want to wait until the National People’s Congress meeting in 2014 is over, before taking any rating (downgrade) decision. However, based on the government’s record thus far on re-balancing, the case for a downgrade of China debt already exists.

It was some time in 2007 when the former Prime Minister Wen Jiabao called the Chinese economy increasingly unstable, unbalanced, uncoordinated and ultimately unsustainable. Not much has improved since then. If anything, China’s economy has become more unstable and unbalanced. This is what Fitch ratings had to say on the China macro situation:

Capital formation rose to account for 48.1% of GDP in 2012 - unprecedented for any large emerging market. If investment continues to grow faster than GDP, it would soon exceed domestic savings (50.8% of GDP in 2012) - and China would sink into a trade deficit, dependent on capital inflows to fund growth. Fitch believes the authorities are determined to avoid such an outcome.

Investment and debt are closely connected and Fitch believes China has a debt problem to match its extraordinarily high investment rate. The stock of debt in China's economy has surged to around 200% of GDP at end-2012 from 129% at end-2008 when the authorities unleashed a credit-fuelled stimulus. The agency believes no economy can operate indefinitely with a rising leverage ratio - another reason why growth is on an unsustainable path.

There has been no progress in rebalancing the economy away from investment towards consumption, year to date. Investment contributed 4.1 percentage points (pp) of China's 7.6% growth in H113, against 3.4pp from consumption. Credit continues to grow faster than GDP: the flow of new "total social financing" was up 30.6% year-on-year in H1 2013 while nominal GDP rose by 8.8%. Fitch believes China faces a process of structural economic adjustment - which could be bumpy. Moreover, some of the costs of fixing China's debt problem are likely to fall on the sovereign.

Source: http://www.fitchratings.com/creditdesk/press_releases/detail.cfm?pr_id=805012

In August, Total Social Financing (TSF) was up by Yuan (CNY) 1.6trn. Consensus forecast was for an increase of just CNY 950bn. In September, TSF rose again by another huge amount – CNY1.4trn. China’s macro-economic turnaround in the third quarter has been entirely due to another round of credit flood.

Such huge numbers on new credit creation (these are ‘flow’ of new credit created every month and not stock of credit) have persuaded some analysts that these numbers might be overstating the actual credit creation and that some double counting might be involved (see http://bloom.bg/193v6g5). However, Fitch has a response to this:

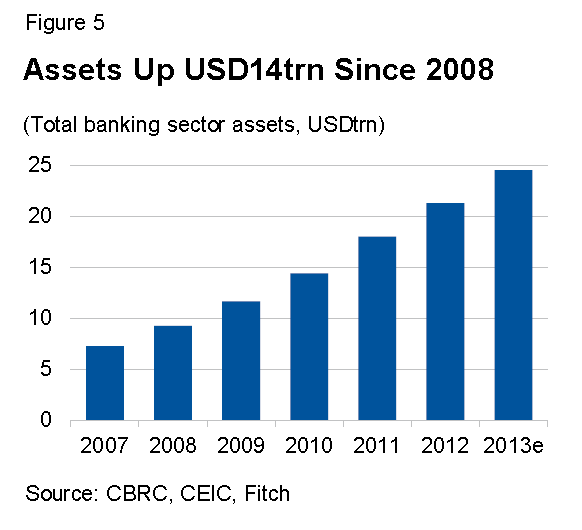

Some double-counting is inevitable, but limited and offset by the numerous channels of credit not captured by either metric, e.g. corporate credit transformed into interbank claims, inter-company credit and payables, private equity (PE) funds (particularly local government PE funds), and person-to-person lending. This is further supported by the fact that growth of total banking sector assets remains so strong (Figure 5), which would not be the case if TSF data contained substantial double counting or diverged visibly from broader financial sector trends.

In Fitch’s view, the principal reasons why credit continues to outstrip GDP are: 1) the majority of non-household principal obligations falling due are being rolled over/refinanced, resulting in a fall in net repayments of credit and propping up credit flows; 2) as the stock of credit rises, an increasing share of new financing is going toward servicing interest payments, which has little or no impact on the real economy; and 3) a substantial portion of credit is going toward long-term projects that have yet to come on line.

Source: ‘Chinese banks - Indebtedness Continues to Rise, With No Deleveraging in Sight’, FitchRatings, 18 September 2013

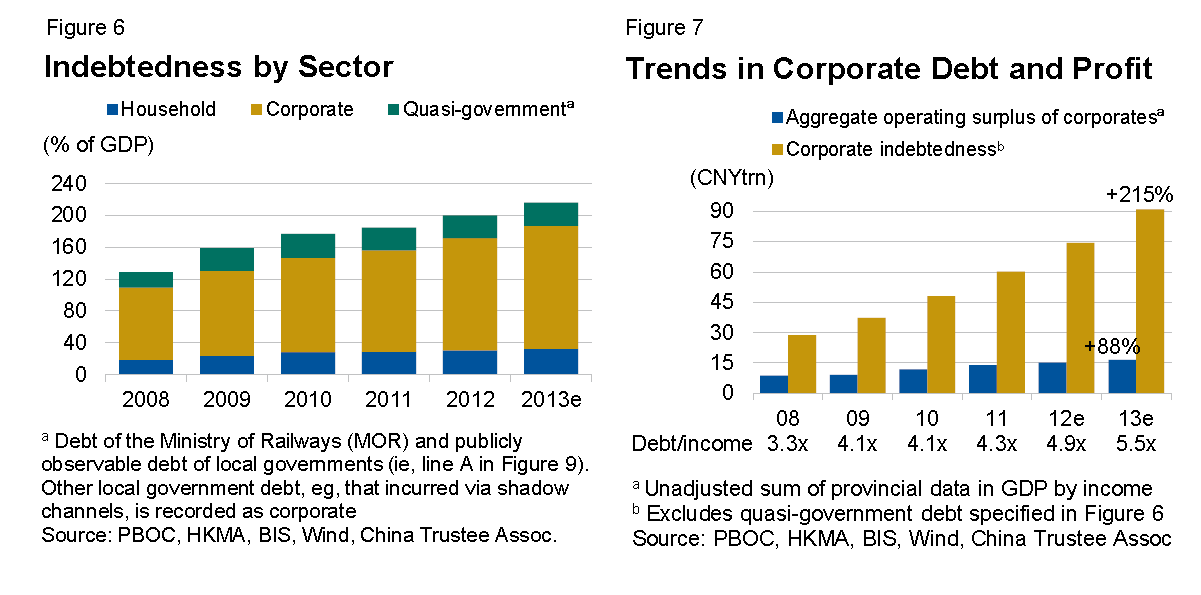

We present below some charts that tell their own story.

“Credit/GDP will have risen an estimated 87pp in the five years ending in 2013, nearly twice that observed in other countries prior to financial sector stress”.

Source: ‘Chinese banks - Indebtedness Continues to Rise, With No Deleveraging in Sight’, FitchRatings, 18 September 2013

Source: ‘Chinese banks - Indebtedness Continues to Rise, With No Deleveraging in Sight’, FitchRatings, 18 September 2013

Source: ‘Chinese banks - Indebtedness Continues to Rise, With No Deleveraging in Sight’, FitchRatings, 18 September 2013

Source: ‘Chinese banks - Indebtedness Continues to Rise, With No Deleveraging in Sight’, FitchRatings, 18 September 2013

China calling on the United States to behave responsibly was clearly a case of the pot calling the kettle black. China’s suggestion that it was time the world abandoned the U.S. Dollar as the global reserve currency might be a reasonable one but certainly, the alternative is not the Chinese yuan. In fact, presently, the Euro looks a safer bet than either the US dollar or the yuan. However, there is a big question mark hovering over sustainable economic growth in the Eurozone.

Finally, when central banks are the only game in town – they are the plaintiffs, the jury, the judge and the executioner – it is foolish to try to view asset prices through the prism of economic fundamentals.

During a brief interview on FOX Business, David Stockman, the author of The Age of Deformation exclaimed "There’s no one in the stock market today except drugged-up day-traders and robots... This is utterly irrational." The blame (and benefactors) are clear, he blasts, "how could someone in their right mind believe that you can have interest rates... at zero for nine years? ... That is the greatest gift to the speculators, to the 1%, to the leveraged traders, to the carry trade ever imagined!" He concludes, "we're almost on the edge of another explosion at the present time." (http://www.zerohedge.com/news/2013-11-07/david-stockman-blasts-brace-explosion-mother-all-bubbles). Enough said.

Published Date: 12th November 2013, Image source: http://1.bp.blogspot.com

-

The Indian stock market has experienced a remarkable surge in mar

-

On September 2023, JP Morgan announced that it will include India

-

Last month, a leading multinational German investment bank publis

-

E-Commerce globally is on the rise. Relentless innovation in tech

-

The state government of Uttar Pradesh is working diligently to gr

-

The contribution of services sector[1] to the Indian economy is w

-

US President Harry Truman entangled in an array of economic view

-

The year 2022 will go down in history in which the great power ri

Post new comment