More often than not, the most objective and well-analysed piece of writing is not possible when a crisis is unfolding. The tendency of journalists and analysts will be to rush information to their readers and clients, respectively. There will be less time for reflection. A far clearer and perceptive analysis will become available, over time. Alternatively, it may be worth perusing stuff that was written well before a crisis happened. For example, if someone had warned of Evergrande well before the s**t hit the fan this year, then that would or should carry a lot more weight. I came across one such article published in the Wall Street Journal in July 2020. The article relied quite a bit on research by Goldman Sachs.

Some key extracts from that article:

Now, another article published on the 10th October 2021, citing research by Nomura Holdings, mentions the USD5.0 trillion debt that Chinese developers carry. In 2020, it was the value of housing including inventories, measured at USD52.0 trillion.

Straight off the bat:

Another article in the same newspaper that appeared a week earlier had this important data point:

The scale of Evergrande’s ambitions was staggering. As of the end of last year, the property developer had more than 700 projects under construction, covering 132 million square meters of total floor area. For comparison, the total floor area of the Empire State Building is about 257,000 square meters.

It is even difficult to make an objective statement on whether Evergrande will or will not be Lehman Brothers for China. Let us not forget that the United States arranged sale and unwinding of many other institutions during the crisis. With Lehman, either they took a chance or were forced to or it might have involved some other political and inter-personal dynamics (Dick Fuld was not a popular man on Wall Street) or some combination of all three.

Allowing it to fail brought America to its knees. Well, Paulson did beg China to bail out its banks (ref.: Paul Blustein's 'The Schism'). No surprises that China is now unimpressed with American swagger and dominance.

But, Lehman Brothers was allowed to fail and it nearly brought America to collapse because a financial institution has far too many linkages above the line and it had below-the-line contingent exposure on derivative contracts. It was a house of cards and so was the broader American financial sector.

Looks like Evergrande is a rather good match.

If the government in China decided not to let Evergrande fail, it will take a lot of money to shore up household balance sheets, local government revenues and much more.

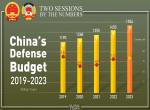

Cue, China's fiscal deficit. Here are some 'official' estimates:

Mind you, all these estimates are excluding Evergrande and property sector bailouts that are yet to be finalised and announced. At the minimum, the ratings outlook must be downgraded, if not the rating itself.

Amidst all this, there are important political developments. It is possible to present the developments in China in the last one year, starting with Alibaba and Jack Ma, as those relating to regulation of businesses with the most recent proposal being the banning of private capital in Chinese media companies. However, that is not the case. They are more than that. In a country where information is hard to come by and where a word added or dropped or a specific word deployed carry meanings that are not immediately obvious to the lay reader, it is important to defer to seasoned observers. So, it is useful to read LingLing Wei in Wall Street Journal and Richard McGregor in Nikkei Asia.

Let us start with LingLing Wei's article in the Wall Street Journal. Key extracts from that article:

- A number of countries closely regulate industry, labour and markets, set monetary policy and provide subsidies to help boost their economies. In Mr. Xi’s version, the government would have a level of control that would allow it to steer the economy and industry along a path of its choosing, and channel private resources into strengthening state power.

- Before this year, Mr. Xi was distrustful of capital, but he had other priorities. Now, having consolidated power, he is putting the whole government behind his plans to make private business serve the state.

- Early this year, when Facebook Inc. and Twitter Inc. took down former U.S. President Donald Trump’s accounts, Mr. Xi saw yet another sign America’s economic system was flawed—it let big business dictate what a political leader should do or say—officials familiar with his views said.

- A few months later, when the Chinese Communist party celebrated its centenary on July 1, Mr. Xi donned a Mao suit and stood behind a podium adorned with a hammer and sickle, pledging to stand for the people. After the speech, he sang along with “The Internationale” broadcast across Tiananmen Square. In China, the song, a feature of the socialist movement since the late 1800s, has long symbolized a declaration of war by the working class on capitalism.

- To Mr. Xi, said Chinese officials, the sight of connected people getting rich could hurt the party’s standing among the underprivileged it is supposed to represent.

- Mr. Xi and his underlings still talk about the need to develop the private sector, which accounts for 80% of China’s urban jobs. But officials say the focus now is on fostering small and midsize companies, in areas ranging from power equipment to sensors and semiconductors, that aren’t likely to become alternative power bases.

- Underpinning Mr. Xi’s actions is an ideological preference rooted in Mao’s development theories, which call state capitalism a temporary phase that can help China’s economy catch up to the West before being replaced by socialism.

- An ardent follower of Mao, Mr. Xi has preached to party members that the hybrid model has passed its use-by date.

- A 2018 article in the party’s main theoretical journal, Qiushi, or Seeking Truth, laid bare his belief: “China’s practice shows that once the socialist transformation is completed, the basic socialist system with public ownership as the main body is established...[and] state capitalism, as a transitional economic form, will complete its historical mission and withdraw from the historical stage.”

- As Mr. Xi clamps down on capital, his popularity among the party’s original base, the working class and rural poor, appears to be growing, thanks to his initiatives to fight corruption and poverty.

- In Xingguo, a southern county where rocky land makes large-scale farming difficult, Mr. Xi’s portrait hangs on the walls of some residents’ living rooms, space once reserved for pictures of Mao.

I have highlighted the key phrases and portions. We underestimate the extent to which specific events shape our thinking and beliefs. Sometimes, we may not even be conscious of it. The events that took place in Capitol in America on January 6th and the subsequent banning of Trump from social media by private companies must have clearly shaken Xi because it shook many other world leaders. It laid bare the power of capital over the power of the State. It could not be possible. Yet, it happened.

Just as Xi picked up the lesson of not letting the Party be weakened by corruption from the collapse of the Soviet Union, the message he picked up from America's financial crisis in 2008 and the treatment meted out to President Trump is that he cannot afford to take chances with private capital. They must be cut to size.

China also took another lesson from international developments. It watched the collapse of the Japan's economy and decided that it was due to Japan wilting under American pressure to strengthen the yen against the US dollar. So, it has done all it could to keep the Chinese yuan from becoming too strong. It may or may not have succeeded but it could not be accused of not trying.

Now, it is always possible to draw the wrong inferences from the experiences of others. It is quite possible that China has done that in all of the three lessons mentioned above.

With respect to Trump and private capital, Chinese capitalists might not be interested in re-imagining and re-fashioning the society as American capitalists are. I doubt if there is a historical precedent in China. There is plenty in America. Of course, historical precedents might not be relevant in a globalised world where Chinese business people receive foreign capital and appoint them to their Boards, leaving themselves susceptible to foreign influence or ‘pollution’ as the Chinese Communist Party thinks. They may be more susceptible to such influences than before. But, the society's long-running ethos does not lend itself so easily to such adventures.

In his landmark book, 'Plagues and People's, Prof. William McNeill writes of China:

Political unity comes easier to a land accustomed from antiquity to regard imperial centralization as the only rightful form of government (p.215)

Second, with respect to the lessons from the collapse of the Soviet Union, it is possible that the excessive centralisation of power in the hands of the party might kill off the dynamism that a limited exposure to capitalism had engendered. Is it possible to turn off and on these switches? Second, corruption related purges suffer from lack of transparency, absence of due process and hence arbitrariness. Therefore, the resentment they create might prove costly later.

Third, with respect to the exchange rate, China might have succeeded in preventing the currency from appreciating against the US dollar especially between 2003 and 2008 when the pressure on the currency to strengthen was at its highest. But at what cost? In order to do so, it had to engage in quantitative easing of its own, by using the Yuan money supply to buy foreign Government debt. So, the dollar might be America's currency but it was China's problem, especially in 2008. It led to China keeping interest rates artificially low to render the currency unattractive for speculators engaging in 'carry trade' – borrowing in low interest rate currencies and lending in higher interest rate currencies. That, in turn, led to rampant domestic credit growth and pervasive capital misallocation. The debt burdens carried by the property developers and the value of the real estate holdings are proof of that.

As though that is not enough, Goldman Sachs, in a recent report, has estimated that China's local governments carry a debt burden equivalent to 50% of GDP:

The total debt of local government financing vehicles rose to about 53 trillion yuan ($8.2 trillion) at the end of last year from 16 trillion yuan in 2013, the economists wrote in a report. That’s equal to about 52% of gross domestic product and is larger than amount of official outstanding government debt. [Link]

Finally, to keep interest rates low, China had to keep domestic prices low, many a time artificially.

Electricity tariffs are regulated. Power generation companies are losing money for every kilowatt hour of electricity sold. They have less incentive to generate power, unless coerced, of course. Then, coal miners are fearful of criminal prosecution and even death sentences for mining accidents. As a result, China has a power shortage now. That is what Professors Alex Yang and Angela Zhang write for 'Nikkei Asia'.

[Parenthetically, however, Eryk Bagshaw of 'Sydney Morning Herald' says that China is shutting off power to its most inefficient and polluting users and hence the current power shortage to certain provinces and firms is a short-term pain that should result in long-term gain. Well, since the denouement is in the uncertain future, it is hard to know if he would be proven right. But, as it appears in the cases of Evergrande and property developers, more generally, this too could be too much too late.]

So, it is clear that in all the three instances, China may well have learnt the wrong lessons or, to put it differently, the lessons it learnt and the 'mistakes' it sought to avoid, may have come at a very high price; too high, in some cases.

In short, China is failing not because it emulated the West but it sought to avoid the mistakes of the West and committed its own, in the process. Now, it seeks to pursue a third way as Ling Ling Wei wrote in the Wall Street Journal, cited above. It embraced capitalism for around forty years (slightly less). Now it wants to switch it off and focus on socialism or common prosperity, for several reasons. Such a 'third way' has not been attempted before. It may not be possible to shut down capitalism and embrace socialism without also killing the economic dynamism that accompanied the dalliance with capitalism.

There may be a lot of sympathy even in the West for China's attempts to shut down the vulgar manifestations of capitalism but it is hard to conclude that the government has been driven solely by such economic and public purpose considerations. So, both from the political and economic angles, success is far from assured.

As I wrote in a column recently, China might have left the barn door open for too long, particularly with respect to reining in debt accumulation by its property sector, local governments and other state-owned enterprises.

Therefore, such formidable, if not insurmountable, politico-economic challenges carry with them the risk that China turns adventurous externally both to divert attention and also to garner the critical resources that might be needed to fix some of these problems.

Into this potent cocktail, Hal Brands and Michael Beckley add something that is quite reasonable in the light of the facts surveyed above. That something is the conclusion that China is a declining power and that that is what makes it more dangerous. In their view, it is wrong to assume that China is an aspiring and rising power threatening the dominance of a status quo power. China's long rise is to be followed by the prospect of a sharp decline and that is what makes China dangerous.

Among their conclusions,

China will be sorely tempted to use force to resolve the Taiwan question on its terms in the next decade.

Interestingly or disturbingly, Gideon Rachman reaches the same view through a different lens:

Both China and the US increasingly feel as if they are engaged in a potentially deadly poker game over Taiwan, as they attempt to bluff each other into backing down. Strategic ambiguity has kept the peace for decades. But a dangerous moment of clarity may be approaching.

In conclusion, a lot is riding on how China's property sector woes and its more general debt problem are resolved or not. Both possibilities present the scenario of enfeebled fiscal conditions and lower economic growth going forward. In turn, it can only mean that the inevitable surfacing of the consequences of China's debt binge of the last fifteen years might turn out to be calamitous geopolitically.

(The paper is the author’s individual scholastic articulation. The author certifies that the article/paper is original in content, unpublished and it has not been submitted for publication/web upload elsewhere, and that the facts and figures quoted are duly referenced, as needed, and are believed to be correct). (The paper does not necessarily represent the organisational stance... More >>

Image Source: https://www.thehindubusinessline.com/news/world/china-evergrande-bondholders-in-limbo-over-debt-crisis/article36645093.ece

-

Introduction The northeast region of India has been inflicted

-

Indian foreign policy under the Modi government has been characte

-

The general elections for the National Majlis (Parliament) of Mal

-

India possibly can boast of having one of the largest (nearly 35

-

Following the visit of an Indian delegation to Afghanistan in Mar

-

The plenary sessions of the Chinese People’s Political Consulta

-

Background Chief of Army Staff (COAS) of the Indian Army, Gene

-

Premise This work attempts to analyse the following premise:-

Post new comment