“With uncertainty, there is never a dull moment.” - Haresh Sippy

Donald Trump’s presidency has sparked fears of a changing world order and an alleged further decline of the US. The ‘America First’ emphasis and the recent US hike of tariffs have disrupted the established system across the globe. The common rationale offered by analysts is that the US is increasing protectionism and turning inward due to internal challenges and perceived threats from China’s rising influence. Foxconn Chairman Terry Gou noted that “what they (US and China) are fighting is not really a trade war, it’s a tech war. A tech war is also a manufacturing war1.” This economic dissension is further interspersed with China’s rapid military transformation particularly in the naval and maritime domain. Trump’s hardline economic policies have started a strategic game of attrition of power between China and the US. But is the world really on the cusp of a new power order? Will China surpass the US to become the number one economy?

Borrowing from the business world, a most famous case study is the Swedish Multinational, IKEA’s comprehensive supremacy in the furniture industry that has fascinated many management experts. IKEA’s business policies and strategies are hardly a secret, so why has no other company been able to replicate IKEA’s success? The explanation is the chain-link logic that enmeshes a very unique mix of resources and competencies that are astronomical for any competitor to afford or replicate. IKEA’s adroit coordination of policies has created an integrated design and constellation of activities that are systemically chain-linked. A rival cannot grab business away from IKEA by adopting only one of them and performing it well. Also, the expertise in one activity/ link cannot be easily carried over to expertise at the others2. The key to the long-reigning US supremacy is also a series of economic, financial, legal, technological, military and diplomatic chain-linked activities that are maintained at a high level of quality, each benefiting from the quality of the other and the whole being resistant to any easy imitation.

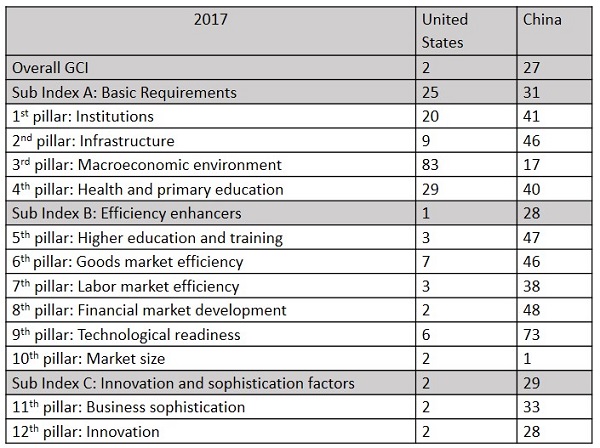

The World Economic Forum’s Global Competitiveness Index (GCI) tracks the performance of close to 140 countries on 12 pillars of competitiveness through an annual report since 2004. GCI assesses the factors and institutions (identified by empirical and theoretical research) that are determining elements for improvements in productivity, which in turn is an essential factor and main determinant of long-term growth and prosperity3. The US ranked 2nd overall for 2017 (below Switzerland), displaying a constant improvement in score since 2010. The strength of the US is attributed to its performance in efficiency enhancers and innovation and sophistication factors, where it comes in at 1st and 2nd respectively. These two sub-indexes reflect sound and well-functioning factors of production and product markets and a vibrant innovation ecosystem in the United States4. China ranked 27th overall in 2017. China reportedly made progress from previous year (2016) in all pillars except its macro-economic environment and infrastructure (an irony for the country leading the biggest financial lending program for infrastructure – the Belt and Road Initiative). The largest gains for China were observed in technological readiness, owing to higher information and communication technology penetration and the extent to which foreign direct investment has been in bringing new technologies to China5.

Even if we were to bring in statistics, the GDP (Gross Domestic Product), GDP PPP (GDP Purchasing Power Parity), GDP per capita etc. the US is ahead of China by more than many miles. At the same time, one must raise concern on the issue of fudging of statistics by China. According to Wikileaks (2010), in 2007 Premier Li Keqiang (when he was the Communist Party head of Liaoning), at a dinner with then US Ambassador to China, Clark Randt, had said that he did not trust the province’s GDP numbers and looked at railway cargo, electricity generation and bank loans to get an idea of the economic activity6. Coming back, the economic gap cannot be bridged by faster running in coming years by China (unless the US was to significantly slow down). The closest any country’s economy came to the US economy was Japan in 1995 when its GDP was a whopping 71.15% of the US GDP (1995, US GDP- $7.66 trillion, Japan GDP- $5.45 trillion). In fact, during the heydays of the US-Japan trade friction era in the 70s and 80s, when the US pressurized Japan to decrease its trade surpluses, the Japanese economy was only a third to half of the US economy.

Chinese GDP in 2017 was 63.12% of the US GDP (2017, US GDP- $19.39 trillion, China GDP- $12.24 trillion). In 2017, the trade deficit in goods trade between the United States and China was $375 billion. Ironically, the US runs a trade surplus in services with China amounting to $40 billion in 2017. In fact, the US has a steadily rising global trade surplus in services amounting to $256 billion in 2017. In regards to GDP PPP, China ranks ahead of the US (2017, China GDP PPP- $23.3 trillion, US GDP PPP- $19.39 trillion). However, GDP PPP figures confer no advantage to China. If the GDP of country A is half that of country B, but the cost of living is also half as much, PPP-adjusted GDP would be equal. Simplifying, PPP aims to measure how much stuff people can buy, rather than just how much money they spent buying it. Further, with China’s exchange rate manipulation, its GDP PPP figures are more a quantitative measure rather than qualitative indicator. Additionally, the GDP per capita, GDP PPP per capita and disposable income figures indicate the mammoth difference between the US and China. While the GDP PPP per capita income of China is $16,000, for the US it is about $60,000. In nominal GDP per capita, the Chinese figures decline even further to a disappointing $8,8007.

With a debt-ridden economy, China aims to transition from investment-driven to a productivity and consumption driven economy. Today, services (52.2 per cent) comprise a larger share of China’s GDP than industry (39.5 per cent) 8. However, China cannot shift to a consumer economy on the scale of the US. Even if the current growth in consumption continues in China, changing demography will bring the inevitable slowdown. The country already faces a serious gender imbalance, combined with a rapidly ageing population. Shockingly, China is world’s lowest ranked country with regard to the gender gap in its sex ratio at birth9. Moreover, the median US household income surpasses the Chinese disposable income per household by a factor of 5-7. As indicated by the above GCI index, though China may rank ahead of the US as number one in market size, it is truly the US that has real market consumption capacity. On the issue of renminbi replacing the dollar as global reserve currency, data released in February 2018 from Swift, the global interbank system, showed that just 1.61 percent of domestic and cross-border payments processed in December were denominated in renminbi. With a 260 per cent debt-to-GDP ratio and a potential trade war with the US, any sudden changes in the value of the renminbi may spark a national bankruptcy.

To escape the middle-income trap, China has made far-reaching efforts in its R&D to build its own advantages and capabilities in the emerging high-tech and upstream sectors as other developing countries catch up. In 2016, the number of international patent filings lodged with the World Intellectual Property Organization rose 45 percent to 43,000 – more than any other country except Japan or the US, which China is set to overtake if current trends continue10. State-led innovation efforts such as the Made in China 2025 and Innovation Driven Development Strategy have focused hugely on new technologies such as Artificial Intelligence, Robotics, Quantum Computing, New Energy Vehicles etc. However, as the Soviet experience showed a state-led innovation model inevitably spirals to a military stronghold that is unable to understand or alter the existing market. Political scientist Hans-Werner Sinn had argued in a 1997 research paper, “If governments stepped in where markets failed, reintroducing markets through the backdoor of systems, competition will again result in market failure11.”

Presently, the nature of innovation in China still has been more towards sustaining technologies rather than disruptive technologies. China competes in markets created by largely western technologies, trying to move from the voluminous low end to the profitable high end. With a huge domestic market that is tightly controlled and monitored, the American Facebook may become the Chinese WeChat and the American Uber is the Chinese Didi Chunxing. The Hong Kong IPO debut of Xiaomi in early July this year has raised doubts over the listing prospects for other Chinese tech groups and the boom in private valuations enjoyed by the sector. Xiaomi, which debuted at half the $100 billion valuation it originally sought, illustrates the risks surrounding the great China tech boom12. Thus, the constant media hype on trade issues presently illustrates a very narrow spectrum of analyzing a country’s economic prospects. The only other GCI pillar after market size where China does better than US is the macroeconomic environment. Despite his far reaching tax reform, Trump’s presidency may see a further decline on that pillar due to his alienating policies even towards allied and friendly countries.

Summarily, the US economy has a mammoth leap over the Chinese economy. Although China has sought to imitate certain links, it very unlikely to be able to replicate the entire constellation of activities that give the US its numero uno position in the world economy. In coming time, China will have to allow more de-regulation, while pursuing a less antagonistic and aggressive foreign policy to maintain the competitive advantages it has built up. Although the Chinese Communist Party has quietly sought to transform into the consolidated China Inc., it has to be wary that re-directing state resources at will, may lead to the downfall of the vibrant Chinese economy.

(The arguments are based on WEF's GCI index. China, in per capita terms, is unlikely to surpass US in near future but it is inching towards catching up. It may not catch up with the US on many of these parameters. But it may enhance its influence in the world despite being low on the GCI. No one say that Japan or Germany, better than China on GCI, have more influence than China. – Ed-in-Chief).

Endnotes:

- Reuters: Taiwan's Foxconn calls Sino-U.S. trade spat a 'tech war', June 22, 2018, https://www.reuters.com/article/us-foxconn-strategy/taiwans-foxconn-says-biggest-challenge-is-u-s-china-trade-war-idUSKBN1JI06H

- Rumelt, R. P. (2011). Good Strategy, Bad Strategy: The difference and why it matters. New York: Crown Business.

- World Economic Forum: The Global Competitiveness Report, 2017-18, http://www3.weforum.org/docs/GCR2017-2018/05FullReport/TheGlobalCompetitivenessReport2017%E2%80%932018.pdf

- World Economic Forum: GCI US profile- http://reports.weforum.org/global-competitiveness-index-2017-2018/countryeconomy-profiles/#economy=USA

- World Economic Forum: GCI China profile- http://reports.weforum.org/global-competitiveness-index-2017-2018/countryeconomy-profiles/#economy=CHN

- Reuters: China's GDP is "man-made," unreliable: top leader, Dec 6, 2010, https://www.reuters.com/article/us-china-economy-wikileaks/chinas-gdp-is-man-made-unreliable-top-leader-idUSTRE6B527D20101206

- All statistics are World Bank figures.

- https://www.cia.gov/library/publications/the-world-factbook/fields/2012.html

- http://www3.weforum.org/docs/WEF_GGGR_2017.pdf

- World Economic Forum: 10 astounding facts to help you understand China today, 24 Jun 2017, Ceri Parker, https://www.weforum.org/agenda/2017/06/10-astounding-facts-to-help-you-understand-china-today/

- https://www.livemint.com/Sundayapp/FP32Ew8uSsTsk40EfG5DuN/Why-competition-may-sometimes-be-harmful.html

- Financial Times: Euphoria around China tech clashes with reality, July 13, 2018, https://www.ft.com/content/95285120-8593-11e8-96dd-fa565ec55929

(The paper is the author’s individual scholastic articulation. The author certifies that the article/paper is original in content, unpublished and it has not been submitted for publication/web upload elsewhere, and that the facts and figures quoted are duly referenced, as needed, and are believed to be correct). (The paper does not necessarily represent the organisational stance... More >>

Image Source: https://cdn.cnn.com/cnnnext/dam/assets/160324233315-on-china-economy-by-the-numbers-00002517-full-169.jpg

{kind=link}

-

Introduction When Cape Town in South Africa faced a severe wat

-

India and Denmark are natural partners connected by common democr

-

“Nuclear governance is now facing massive challenges. In the la

-

After COVID-19, certain signs of economic recovery are being visu

-

Prime Minister’s War Aims Even before the blood-stains coul

-

US Secretary of State Anthony Blinken's three day (April 24-26) v

-

Goa’s Aguad Port and Jail Complex in Sinquerim have been in the

-

Introduction Foreign policy, as an instrument to promote nati

Post new comment