wer.jpg

wer.jpgThe Vivekananda International Foundation recently organized a talk by Dr. V. Anantha Nageswaran on the Union Budget 2020-21 and the macroeconomic challenges that the country faces. Dr. Nageswaran is a member of the Prime Minister’s Economic Advisory Committee. He is a Distinguished Fellow at VIF and a senior economist with a vast body of work in the finance and management sector.

Dr. Nageswaran began by emphasizing that the Union Budget should be considered in context of the inherent non-linear and asymmetric relationship that exists between Government policy and macroeconomic variables. He asserted that given the difficult economic situation, this year’s budget managed to strike a balance and did not cause any harm to the natural forces of economic recovery in the country.

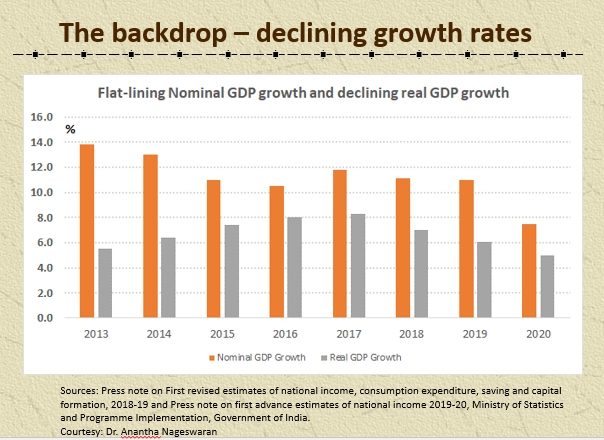

In addition to an uncertain global economic scenario, this year’s budget also came against the backdrop of decelerating momentum of GDP growth (Fig. 1), and declining savings and investment rates. India’s gross fixed capital formation as a percentage of GDP has come down from 34% to 28-29% (Fig 2).

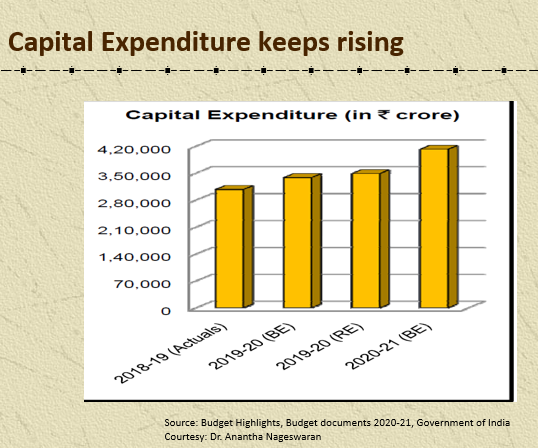

Additionally, a global slowdown in emerging market economies leading to low demand, coupled with declining risk appetite of private sector has weakened the engines of economic growth-ie. exports growth and capital formation. Given the high fiscal deficit levels, there is very little that government can actually do to revive demand and subsequently growth. In this context, the Government’s move to budget a higher capital expenditure this year to stimulate the market should be seen as a positive step to set the ball rolling (Fig 3).

Micro fixes over Big Bang Reforms for dealing with the slowdown

Improving the business environment is crucial for economic recovery, especially for MSMEs. In Budget 2020-21, the Government has proposed: extension of invoice financing to MSMEs through TReDs, a scheme to provide subordinate debt for entrepreneurs of MSMEs, and a scheme anchored by EXIM Bank and SIDBI to handhold MSMEs in export markets.

In this regard, the Government is also reforming its taxation regime. In 2019, it enacted the provision to lower corporate taxes to 15% for new domestic companies in manufacturing and power sector last year. Union Budget 2020-21 further proposed tax benefits to start-ups, and concessions for Sovereign Wealth Funds. Changes with respect to turnover threshold and exemption limit are further medium-term positive policy changes towards reducing the compliance burden on small retailers, and traders that constitute the bulk of MSME sector. The proposed direct tax slab rates (without exemption) is another positive step towards subsequent simplification of the taxation structure.

According to Dr. Nageswaran, it is such incremental reforms that impact the business environment for SMEs and pave the road for sustainable growth recovery. Going forward, ironing out wrinkles in GST norms for greater compliance, and ensuring access to working capital should be on the reform agenda.

Financial Sector Reforms:

Acknowledging the need for financial sector reform, Dr. Nageswaran said that increasing the deposit insurance cover from Rs.1 Lakh to Rs.5 Lakh per depositor, was a positive step towards boosting sentiment and reducing stress in the sector. Additionally, eligibility limit for NBFCs for debt recovery under SARFAESI Act proposed to be reduced to asset size of Rs.100 crore or loan size of Rs.50 lakh; and separation of NPS Trust for government employees from PFRDAI are other significant financial reforms undertaken by the Government. These, coupled with the under-consideration resolution framework for financial Institutions, would not only reassure small deposit holders about the safety of their deposits, but also avoid the risk of systemic failures.

In dealing with the crisis in banking sector, India needs to strike a balance between public sector and private sector ownership to ensure more accountability and good governance in the financial sector. Using the recommendations in the PJ. Nayak committee report of 2014 as a blueprint, large public sector banking framework can be retained, with sustained efforts to have improved management, efficiency and governance culture in banks. In this regard, the budget proposal to sell government’s holdings in the IDBI sector is a welcome step and can be used to test this model.

In terms of revenue, receipts from government disinvestment estimate of about Rs. 2.1 lakh crore would depend upon the sentiment in global financial markets. With the current state of uncertainty in the financial markets - exacerbated due to COVID19 outbreak – significant risk remains embedded in the deficit numbers for this year. The government expects to see an uptake in tax revenue from increased compliance due to budget proposals such as Vivaad-se-Vishwas scheme, and waiver of interests and penalties etc.

Dr. Nageswaran also pointed out that since Indian bond markets have been favourably disposed post-budget, the government’s borrowing costs remain low.

The second part of Dr. Nageswaran talk focused on the broader macroeconomic challenges facing both Indian and Global Economy. Indian economy is currently in the midst of a twin financial crises – one stemming from both the banking as well as the non-banking financial sector. Growth revival after such a financial crises where both borrowing and lending sentiment is low, would require much longer, and can have lasting negative effects. In order to chart the path for sustainable growth, Dr. Nageswaran suggested:

Risky to Resort to Debt

While tackling such a crisis, Dr. Nageswaran reiterated that it is crucial to exercise restraint in borrowing from the capital markets. The disciplining role of debt is limited, especially at a time when global financial sector as a whole is facing uncertainty. The moral hazard from larger borrowers defaulting and then the central banks having to bail them out due to the fear of “too big to fail”, remains significantly high.

Prioritize Savings rather than Consumption

On the trend of investment-less growth observed in the developed world over the past few years, Dr. Nageswaran said that while capital markets channel savings into investments in theory, in reality this is impeded by a tendency for short-termism and governance issues in the corporate sector. India needs to learn from this and stay wary of repeating this trend. In order to deal with this, India needs to prioritize household savings formation rather than becoming a consumer-driven economy.

Consolidation of Agricultural Sector

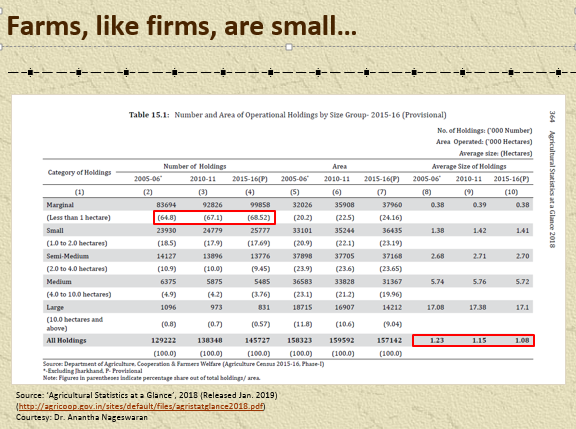

Farm sector in the country is deeply fragmented, with average land holdings of around 1.08 hectares per farmer, and more than two-thirds of all farm holdings falling in the less-than 1 hectare per farmer bracket (Figure 6). (The OECD recommends 4 hectares as the optimum size for a productive farm.) This creates significant distress in the agriculture sector as a whole due to inefficiencies causing small farmers to remain marginalized. Additionally, moving towards a liberalized farm subsidy regime that incentivizes farmers to produce and sell as per the market is the need of the hour. This would also aid in mitigating the inefficiencies regarding indiscriminate power and water consumption by the sector, which results in a downward spiral of crisis.

Formalizing the MSME sector

Like the agriculture sector, the corporate sector is also marked with extreme fragmentation. Companies with Rs. 100 crore or more paid up capital form a miniscule part of the sector (Fig. 8). Bulk of the MSME sector is distressed due to difficulties and high costs of formalization. In addition, higher logistics costs further result in Indian industry lagging competitiveness in international markets. Public policy incentivizing MSMEs to scale-up and increase capacity is crucial for achieving sustainable, productivity-led growth.

Dr. Nageswaran concluded by reiterating that deceleration of growth in India has been a consequence, in large parts, of the crises in the financial sector. This year’s budget has served to aid and not impede the natural forces of economic recovery. Additionally, India needs public policy to address the aforementioned challenges for achieving long-term sustainable growth. Considering these along with the uncertain global economic scenario, Dr. Nageswaran predicted the GDP growth to be around 6-6.5% in the medium term.

The talk was followed by a questions and answers round where participants further deliberated and contributed to the vital discussion.

-

On 19 April, the United Nations Assistance Mission in Afghanista

-

A meeting of the Pakistan Study Group (PSG) was held in hybrid mo

-

On 08 April, the Vivekananda International Foundation (VIF) organ

-

On 15 March 2024, the Vivekananda International Foundation organi

-

On 4 March, the Vivekananda International Foundation (VIF) organi

-

In the emerging quantum world, establishing quantum secure commun

-

The Vivekananda International Foundation (VIF) and Coimbatore Dis

-

On February 21, the Vivekananda International Foundation (VIF) or

Post new comment