Introduction

The 23rd of June 2016, saw the United Kingdom (UK) participate in a referendum as regards to its membership in the European Union (EU). A relatively narrow margin of 52 per cent of the votes tipped the balance in favour of the ‘leave’ campaign and thus set the wheels rolling for Britain’s exit, or ‘Brexit’ from the regional union. The financial markets reacted to the vote, with the British Pound plummeting to an all-time low in 31 years against the dollar and a staggering wipe-out of two trillion dollars of shares globally1.

The domestic political situation was no less striking. The Prime Minister resigned, the opposition leader battled for internal leadership and the Scottish First Minister indicated that Brexit could indeed break-up the UK. 2 The EU member states on the other hand asked for the UK to immediately invoke Article 50 of the Lisbon Treaty that permits an EU member state to withdraw from the union unilaterally. On March 29th, 2017, the UK Prime Minister Theresa May, invoked Article 50 that gave the two parties up to March 29th, 2019, to negotiate exit terms.

The ongoing negotiations are divided into two phases, with Phase One dealing with UK’s financial obligations, the Irish Border and rights of citizens and Phase Two dealing with the framework for future relations with the EU. 3 While much is up for debate, the contrary opinions on key aspects of the terms of withdrawal may lead to a ‘no deal scenario’. Irrespective of the nature of negotiations, a divorce from the EU after 45 years of association is bound to have repercussions on crucial facets that define the economic and socio-political functioning of the UK, as also it’s dynamic with the EU.

This article attempts to briefly analyse the consequences of Brexit on issues that have been outlined in Phase One of negotiations, namely, UK’s Financial Markets and Soft Border Issues with Ireland. Additionally, it seeks to throw light on the impact of the exit on the EU.

Impact on the Financial Services Industry

The financial service sector is of vital importance to the UK. In 2017, it contributed £119 billion to the UK economy, comprising of 6.5 per cent of the total economic output and 1.1 million jobs.4 Furthermore, 30 per cent of the UK’s inward Foreign Direct Investment (FDI) stock is attributed to the financial services sector.5 The EU has hitherto provided a framework within which the UK financial services industry operates, causing deep interlinkages between the two parties. The UK has profited from the European Single Market that facilitated the ‘four freedoms’ of free movement of goods, services, labour and capital. More so the ‘passporting’ regime has been instrumental in the creation of a single market for financial services. 6 It has allowed banks and investment firms in an EU member state to provide services in other member states via the establishment of branches with no further authorisation and licensing requirements. This has enabled the UK to become a global financial centre with a majority of assets coming in from activities conducted in the EU such as trading EU equities. 7

The overall consequences of the departure at this point depend on the conclusion of ongoing negotiations and the agreements made thereafter. Nevertheless, Brexit leads to the termination of EU regulation for the UK, putting it in a position of third-party countries outside the European Economic Area (EEA). With the EU’s financial framework out of play, UK firms would lose their passports under various directives enforcing EU financial law to deliver financial services in the EEA. This could lead to UK firms relocating to the EU-27 (EU member states sans the UK) to retain access to their markets. Looking at banking services in London alone, Brexit would then cause the migration of €1.8 trillion worth of assets outside the UK.8 Given that Brexit is not a ‘zero sum game’, financial activities cannot be relocated from the UK without raising additional economic costs.9 Relocation of financial services would mean the establishment of subsidiaries in the EU to provide the same. As per a February 2018, PwC report, unlike branches, as subsidiaries of financial firms require independent capitalisation, it entails the generation of higher corporate and capital costs leading to a loss in efficiency.10 It means a steep decline in terms of financial profitability as also a reduction in assets that would otherwise contribute a major share to the economy’s GDP.

As another possibility, the firms may choose to pare down their financial activities in the UK and the EU markets. However, this reduction, even if only of commercially marginal activities, would directly lead to a decline in the market liquidity and hence affect the consumers trading activities causing an eventual increase in cost.11

As mentioned, Brexit would mean the loss of passporting rights and shift the UK to the third country position for the EU-27. The EU financial regulatory framework, after a recent legislation, does provide for a third country ‘equivalence’ regime as an alternative to passporting. The equivalence regime enables a non-member to provide services to the EEA if the said country proves to be ‘equivalent’ by EU standards.12 The provision includes directives such as the Markets in Financial Instruments Directive (MiFID) and Alternative Investment Fund Managers Directive (AIFMD) to ensure the same. However, this regime extends to limited services and is also subject to withdrawal if the country deviates from EU standards.13 Therefore, the limited scope and lack of safeguards of the equivalence regime cannot provide a long-term solution to the problem and also would diminish existing financial productivity and output.

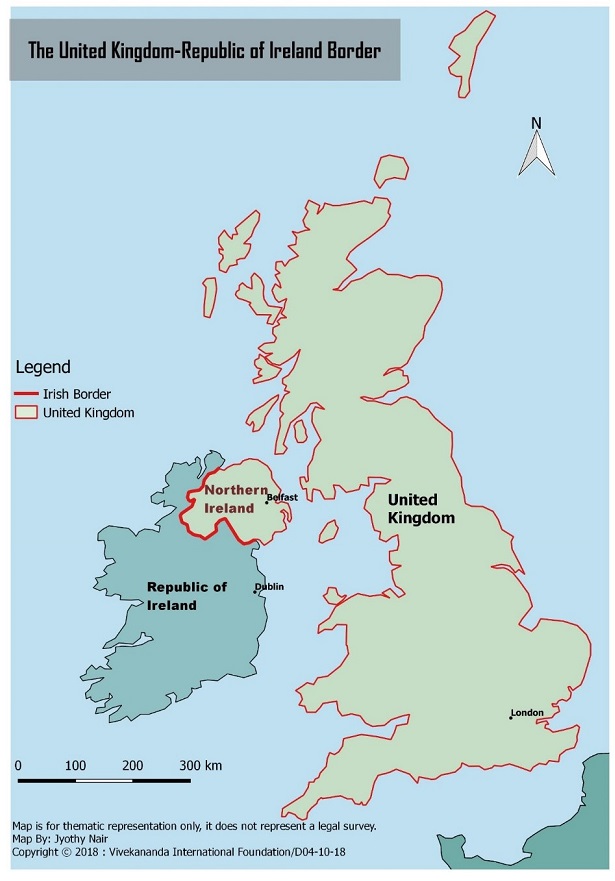

The Irish Border Debate

As a member of the EU, UK’s ‘soft’ borders have been open to trade and human migration. But the June 2016, referendum was representative of how the Britons wanted to redefine control over what or who entered its borders. In essence, this means ‘hardening’ of borders in terms of checks on access for trade and travel. The effect of that on its maritime borders will be critical on the economic front but will have severe socio-economic repercussions on its only overland border – the Irish Border.

The debate of the Irish Border has been widely contested across Brexit negotiations on two fronts – the ramifications on the ‘peace processes’ between the Republic of Ireland and Northern Ireland under the ‘Good Friday Agreement’ and the economic concerns. The land border was drawn in 1921 as part of the peace process between the UK and the Irish who sought independence. Northern Ireland, with a majority of Protestant population, remained a part of the UK and the Catholic Southern part formed the Republic of Ireland. In 1998, the Good Friday Agreement brought about a relief for sectarian tensions that had flared and the border that was once hardened by checkpoints almost became invisible.

Keeping in mind the history, both the UK and the EU have from the onset maintained that they seek to avoid a hard border. As the UK’s 2017, White Paper states, “When the UK leaves the EU we aim to have as seamless and frictionless a border as possible between Northern Ireland and Ireland so that we can continue to see the trade and everyday movements we have seen up to now.”14 However, this is in direct contradiction with certain objectives the British government has outlined for Brexit. The UK wants to practice an independent trade policy and make free trade deals for which it wishes to leave the customs union and thereby the single market. This cannot be done without the implementation of customs checks at borders to adhere to regulatory control, which would mean doing the same for the border with the Republic of Ireland, which will remain a part of the EU after Brexit.

Economically, that would have a far-reaching effect on the Republic of Ireland’s GDP as 15 per cent of its external trading activities dealing with key sectors such as transport and agriculture, are carried out with Britain. 15 Being a WTO member, UK’s divorce from the EU could mean falling back on its trading rules. A government funded study by Copenhagen Economics suggests that this would mean a 7 per cent cut in Irish GDP by 2030. 16 Moreover, the Republic of Ireland’s major routes to reach EU markets transit though mainland Britain.

The Irish border, unlike a conventional territorial border, is a compromise that has brought an end to decades of sectarian violence in the region. Under the Northern Irish peace process, the border has become all but redundant in terms of custom checks and inspection purposes.17 Hardening of the border brings with it the risk of undermining the devolution settlement that has kept the sectarian tensions at bay.

The UK-EU Joint Report of 2017, on Phase One of the negotiations set out three possible solutions to the problem. One such solution is that of the ‘backstop’ option that proposes for Northern Ireland to become a Common Regulatory Area (CRA) wherein it would comply by EU customs rules, free movement of trade and relevant EU market legislation.18 However, this is an incomplete solution. The CRA does not extend to trade in services nor does it avail the preferential tariff treatment under the EU’s Free Trade Agreements (FTA) as they are applicable only to members of the union. This would put Northern Ireland in a no-win situation as it would have to conform to EU legislation and allow unrestricted access to goods from countries with whom the EU has FTA’s but not avail the benefits of the same.19 Besides, complying with EU customs rules could mean not being covered by commitments in UK’s future FTA’s. 20

Overall the economic costs of the CRA would be heavy for both Northern Ireland and the Republic of Ireland.

Impact on the EU

The EU is also set to incur economic costs from the disunion. The UK being the second largest economy of the EU would subtract 16 per cent of the EU’s GDP after it leaves the block.21 With 13 per cent of its population lost and subsequent loss in labour and hence productivity this would no doubt leave the EU poorer.22

An Erasmus University Rotterdam study explains how the countries that have high volumes of trade with the UK will suffer grave costs due to a balance of payments deterrence, especially the Republic of Ireland, Germany and Cyprus. 23 The UK is the second and third largest trading partner of Cyprus and Germany respectively. Moreover, Ireland with 89 per cent oil imports and 93 per cent gas imports from the UK is set to be the biggest loser, cutting off a significant chunk from its GDP.24 Overall even if the UK and EU settle on an FTA, the EU-27 output will shrink by 0.8 percent and employment by 0.3 percent.25

However, the UK has been growing at a slower pace than the EU-27. According to a Financial Times study the low rates of savings and high fiscal debt of the UK has also led to a marginal increase in overall debt of the EU as a proportion to its GDP.26 Thus, the withdrawal will help reduce the debt ratio.

Politically, despite Brexit, it can be observed that there has been a reduction in the influence of Eurosceptic parties.27 However, for the EU smaller states there is always a threat of a shift in the balance of power in favour of Germany who also has the advantage of being the largest economy in the EU.

Finally, there is the impact on migration. Under the current regime, EU nationals are permitted to move and work freely within the EU. Brexit brings this to an end. The UK hosts approximately 3.6 million EU citizens who form a notable portion of its workforce.28 While this indicates loss of labour output for the UK, it also signifies an increase in unemployment of these EU nationals or at least an increase in migration costs in terms of visas.

End Notes:

- Hobolt, S. (2016). The Brexit vote: a divided nation, a divided continent. Journal of European Public Policy, 23(9), pp.1259-1277.

- Ibid.

- Hohlmeier, M. and Fahrholz, C. (2018). The Impact of Brexit on Financial Markets—Taking Stock. International Journal of Financial Studies, 6(3), p.65.

- Rhodes, C. (2018). Financial services: contribution to the UK economy. [online] Researchbriefings.parliament.uk. Available at: https://researchbriefings.parliament.uk/ResearchBriefing/Summary/SN06193 [Accessed 3 Oct. 2018].

- Welfens, P. and Baier, F. (2018). BREXIT and Foreign Direct Investment: Key Issues and New Empirical Findings. International Journal of Financial Studies, 6(2), p.46.

- Pwc.co.uk. (2018). Impact of loss of mutual market access in financial services across the EU27 and UK. [online] Available at: https://www.pwc.co.uk/financial-services/assets/pdf/impact-of-brexit-on-fs-in-europe.pdf [Accessed 3 Oct. 2018].

- Hohlmeier, M. and Fahrholz, C. (2018). The Impact of Brexit on Financial Markets—Taking Stock. International Journal of Financial Studies, 6(3), p.65.

- Sapir, A., Schoenmaker, D. and Véron, N. (2017). Making The Best of Brexit For the EU27 Financial System. [online] Brussels: Bruegel. Available at: http://bruegel.org/wp-content/uploads/2017/02/Bruegel_Policy_Brief-2017_01-090217.pdf [Accessed 3 Oct. 2018].

- European Union (2018). Implications of Brexit on EU Financial Services. Brussels: Directorate General for Internal Policies.

- Pwc.co.uk. (2018). Impact of loss of mutual market access in financial services across the EU27 and UK. [online] Available at: https://www.pwc.co.uk/financial-services/assets/pdf/impact-of-brexit-on-fs-in-europe.pdf [Accessed 3 Oct. 2018].

- Ibid.

- Wyman, O. (2018). The Impact Of The UK’S Exit From The EU On The UK-Based Financial Services Sector. [online] Oliverwyman.com. Available at: https://www.oliverwyman.com/content/dam/oliver-wyman/global/en/2016/oct/Brexit_POV.PDF [Accessed 3 Oct. 2018].

- Ibid.

- HM Government (2018). The Future Relationship Between the United Kingdom and The European Union. London: HM Government.

- Ford, J. (2018). The economic consequences of the Irish border question | Financial Times. [online] Ft.com. Available at: https://www.ft.com/content/84fc0ec0-8298-11e8-a29d-73e3d454535d [Accessed 4 Oct. 2018].

- Ibid.

- McCall, C. (2018). Northern Ireland faces rebordering after Brexit. [online] LSE BREXIT. Available at: http://blogs.lse.ac.uk/brexit/2018/09/17/northern-ireland-faces-rebordering-after-brexit/ [Accessed 4 Oct. 2018].

- Araujo, B. and Pasini, L. (2018). Irish border backstop: many unanswered questions and considerable economic challenges. [online] LSE BREXIT. Available at: http://blogs.lse.ac.uk/brexit/2018/06/05/irish-border-backstop-many-unanswered-questions-and-considerable-economic-challenges/ [Accessed 4 Oct. 2018].

- Ibid.

- Ibid.

- Romei, V. (2018). What will the EU look like after Brexit? | Financial Times. [online] Ft.com. Available at: https://www.ft.com/content/dec6968c-f6ca-11e7-8715-e94187b3017e [Accessed 4 Oct. 2018].

- Ibid.

- Aspegren, E. (2018). The Political and Economic Impact of Brexit on the EU. [online] The Claremont Journal of Law and Public Policy. Available at: https://5clpp.com/2018/02/20/the-political-and-economic-impact-of-brexit-on-the-eu/ [Accessed 4 Oct. 2018].

- Ibid.

- Chen, J., Ebeke, C., Lin, L., Qu, H. and Siminitz, J. (2018). The Long-Term Impact of Brexit on the European Union. [online] IMF Blog. Available at: https://blogs.imf.org/2018/08/10/the-long-term-impact-of-brexit-on-the-european-union/ [Accessed 4 Oct. 2018].

- Romei, V. (2018). What will the EU look like after Brexit? | Financial Times. [online] Ft.com. Available at: https://www.ft.com/content/dec6968c-f6ca-11e7-8715-e94187b3017e [Accessed 4 Oct. 2018].

- Chelotti, N. (2018). Brexit may have strengthened Eurosceptic parties, but there is little prospect of other exit referendums. [online] LSE BREXIT. Available at: http://blogs.lse.ac.uk/brexit/2018/04/30/while-the-brexit-negotiations-strengthened-eurosceptic-parties-across-europe-there-few-prospects-of-other-exit-referendums-taking-place/ [Accessed 4 Oct. 2018].

- The Week UK. (2018). How will Brexit affect immigration?. [online] Available at: http://www.theweek.co.uk/95761/how-brexit-will-change-immigration [Accessed 4 Oct. 2018].

Image Source: http://60811b39eee4e42e277a-72b421883bb5b133f34e068afdd7cb11.r29.cf3.rackcdn.com/2016/06/brexit-1462470589PAa.jpg

{kind=link}

-

Background Chief of Army Staff (COAS) of the Indian Army, Gene

-

Premise This work attempts to analyse the following premise:-

-

Modi is the first and only Prime Minister to place before the peo

-

From being an intensely hated person, he has become the most admi

-

The Jallianwala Bagh massacre on April 13, 1919, in Amritsar, Pun

-

While more than sixty countries around the world will conduct dem

-

Introduction The Indian Ocean Region (IOR) is a vital hub of g

-

On 7 March 2024, Sweden officially became NATO’s newest member,

Post new comment