Agriculture plays an important role in the Indian economy with over 58 per cent of rural households dependent on agriculture for their livelihood. As per the 2nd revised estimates by the CSO, the share of agriculture and allied sector (including agriculture, livestock, forestry and fishery) is expected to be 17.3 per cent per cent of Gross Value Added during 2016-17 (at constant prices).

Growth rates of agriculture production from the 1990’s till the mid-2000’s was lower than that in 1980’s. This was accompanied by withdrawal of institutional support from the Government. This took place in several ways. On account of joining the World Trade Organization in 1995 by India, the protection offered to many commodities from imports weakened, this in turn resulted in fall in output prices of these products. Secondly, as part of the fiscal reforms, major input subsidies were rationalized which in turn resulted in increase in cost of inputs such as seeds, fertilizers, electricity, etc. The rise in input prices was not matched by a corresponding increase in output prices and crop yields and minimum support prices were not available to all farmers, particularly small and marginal farmers. Thirdly, public capital formation in agriculture continued to fall and growth of public expenditure on agricultural research plateaued down (Chart 1).

The agricultural sector also suffered from chronic lack of access to formal credit and insurance which in turn dissuaded the farmers from adopting improved seeds, fertilizers and implements. There was also rise in share of informal source of credit. This in turn resulted in increase in indebtedness due to high rates of interest (Rana Hasan: Sustaining Growth, Ensuring Inclusion, 2017). This note traces the historical evolution with reference to various legislative developments pertaining to rural indebtedness, Central and State legislation, recent debt waivers, and impact on banking sector.

History of Debt Relief in India

During the 19th Century on account of lack of focus of the colonial rulers to the agricultural sector, the Indian sub-continent was subjected to debilitating famines. Consequently, Famine Commissions were appointed and as a follow-up to the reports, two important legislations were enacted – Land Improvement Loan Act, 1883 and Agriculturists Loans Act. As per the Land Improvement Loan Act, it was mandated that long-term loans could be advanced after the authorization of the Central Government which could be repaid in installments. The Agriculturists Loan Act was enacted for short-term credit facilities. In order to regulate the money lending business in the country, the Usurious Loan Act, 1918, was enacted which authorized the Judiciary to relieve the debtors of the liability to pay excessive interest. Similarly, Provincial Acts such as Punjab Relief of Indebtedness Act, 1934, and Bihar Money Lenders (Regulation of Transactions) Act, 1939, were also enacted.

Central Debt Waivers

The alarming levels of indebtedness resulted in the first loan waiver decision taken in 1990 and the Agriculture and Rural Debt Relief Scheme was approved. The scheme was implemented during 1990-91, as per the Report on Task Force of Rural Co-operative Credit Institutions (2006). The total outlay on this scheme was Rs. 100 billion. This debt waiver scheme affected the rural credit scenario adversely with high incidences of defaults and it took banks several years to recover from this situation.

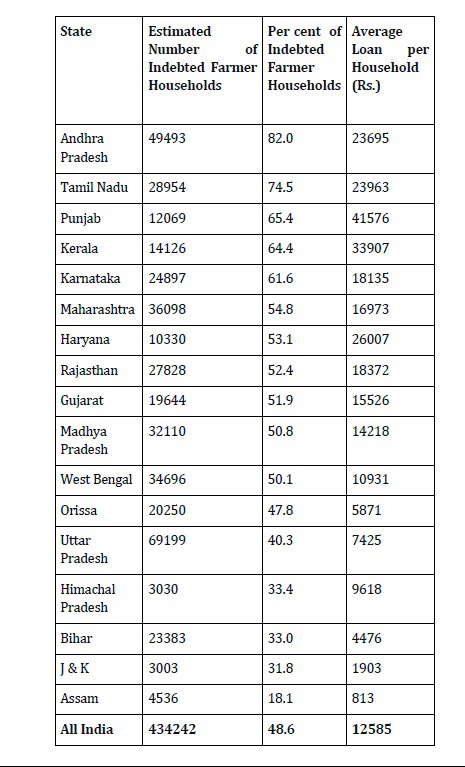

An Expert Group on Agricultural Indebtedness was constituted by Government of India, chaired by Shri R. Radhakrishnan2 in 2007. The report of the group was submitted in July, 2007 and drew the attention of the policy makers towards the findings of the Situation Assessment Survey of farmers conducted by National Sample Survey Organization (NSSO) during January-December 2003, suggesting that 89.33 million farmer households (48.6 per cent) were indebted (Table 1).

This pointed towards the magnitude of the problem at hand. One of the primary recommendation of the group was that concerted efforts should be made to resurrect rural credit delivery agencies in terms of their geographical spread as well as organizational strength. As a follow-up to the report, Union Finance Minister in his budget speech for 2008-09 announced a Debt Waiver and Debt Relief Scheme, although he himself acknowledged that the Expert Group had not recommended debt waiver. It was mandated that all agricultural loans disbursed by scheduled commercial banks, regional rural banks and co-operative credit institutions up to March 31, 2007 and overdue as on December 31, 2007 were to be covered under the scheme.

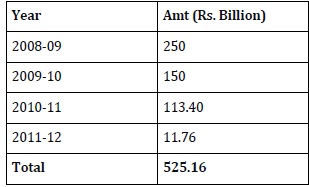

The total value of overdue loans were estimated to be Rs. 500 billion and the OTS relief on the overdue loans was estimated to be Rs. 100 billion. The Agricultural Debt Waiver and Debt Relief Scheme 2008 (ADWRDS) was estimated to cost Rs. 716.8 billion but the actual disbursement towards ADWRDS was Rs. 525.16 billion. The amount waived was much larger than the cumulative credit subsidy (Rs. 245.25 billion) on short-term credit since 2007-08 (Table 2).

As per the CAG report, Government of India waived agricultural loans to the tune of Rs. 520 billion, related to approximately 0.03 billion small/marginal and other farmers. As per the audit, 13.5 per cent of the accounts eligible under the scheme were declared ineligible by the lending authorities whereas 8.5 per cent of those who were ineligible were included. Approximately Rs. 0.21 billion was spent on loans that were taken for non-agricultural purposes. The waiver only targeted formal debt (borrowing from banks) thus benefiting large farmers more than small farmers since smaller farmers are primarily dependent on informal sources of credit. The scheme did not differentiate between those who are willful defaulters and those who are involuntary defaulters. It also did not differentiate between farmers who carry high risks on account of dry conditions and those who are not subjected to vagaries of weather on account of assured irrigation.

The massive write-off of loans took its toll on the banking system and it might have served as one of the important causes for the rise in the Non-Performing Assets (NPA) of the banking system, which had increased three-fold between 2009-10 and 2012-13 (Table 3).

Recently Announced State Loan Waivers

Maharashtra Government had on June 24, 2017 announced agricultural loan waiver for loans taken between April 1, 2012 and June 30, 2016, the time line for agricultural loans was later extended to loans taken from 2009 onwards. It has been estimated that this loan waiver would benefit 8.9 million farmers which would cost Maharashtra Exchequer Rs. 340 billion. In case of Maharashtra, implementation obstacles are being faced since the amount to be waived is to go directly to individual’s farmer account after Aadhaar number verification and some of the farmers may not be having Aadhaar card and may be left-out in the process. This announcement has followed the announcement made by Uttar Pradesh Government to waive farm loans worth Rs. 360 billion. It has been estimated that the impact of this waiver will be to the tune of 2.5 per cent of the State’s Gross State Domestic Product (GSDP).

In case of UP, the Government has dropped its plan of raising finance by floating ‘Kisan Rahat Bonds’ for financing the farm loan waiver scheme and would be financing the loan waiver from it’s budgetary resources. Karnataka has also announced a debt waiver to the tune of Rs. 81.7 billion for farmers availing loans from co-operatives. The latest to join the band wagon of debt waivers is Rajasthan, which has announced waiver of all farm loans up to Rs. 50,000 per farmer. The debt waiver is expected to cost the state govt. up to Rs. 200 billion.

With reference to the spate of loan waiver announcements, it has been clarified by the Union Finance Minister that no support from the Union Government would be forthcoming with reference to such farm loan waiver announcements made by the State Governments. The UP model is expected to serve as a template for other state governments which have announced loan waiver schemes. Assuming all the poll bound states including Gujarat, and Madhya Pradesh too announce farm debt waivers and extend it to one-third farm loans, then the aggregate amount of farm debt waivers before the 2019 elections would increase to Rs. 2 trillion or 1.3per cent of GDP (Table 4).

*Includes bank credit by Scheduled Commercial Banks, Rural Banks and Co-op Banks; Source: Mint Newspaper - Rajya Sabha Question, RBI Handbook of Statistics, CMIE and Mint Newspaper Calculations

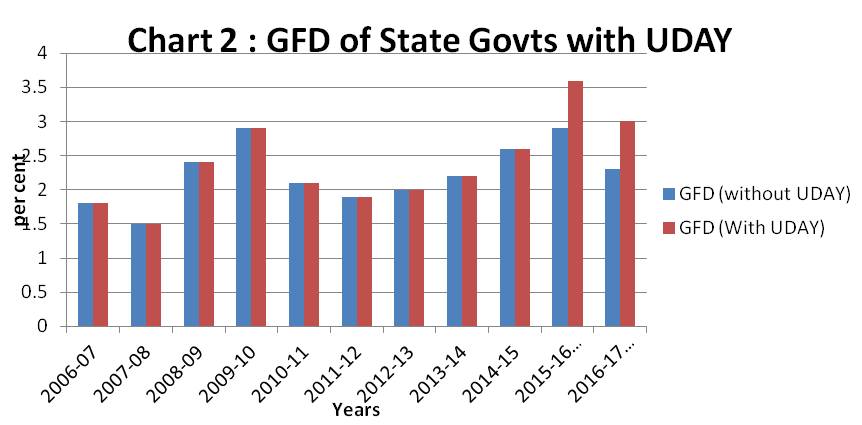

The borrowing requirements of state governments may also increase on account of burden of the debt waivers. This may lead to hardening of yields in the primary issuances. The range of weighted average yields in the primary auctions during the early part of the year 2017 were quite high which subsequently softened during the latter part of the year (Table 5). This may lead to a rise in the interest burden for the states. The State governments gross market borrowings are expected to rise to Rs. 4,500 billion from Rs. 3,700 billion in 2016-17 on the expectation of rising fiscal deficit due to pay revision, servicing of UDAY debt, a spike in debt repayment from 2017-18 onwards and exclusion of most state govts. from investing in NSSF from April 1, 2016. The fiscal deficit of states is expected to be around 3.7per cent of GDP in 2016-17, a 13 year high.

Source: RBI

The combined fiscal position of states deteriorated sharply in 2015-16 (RE) (Chart 2) from the budgeted estimates for the year. For the first time in more than 10 years, the Gross Fiscal Deficit (GFD)-GDP ratio at 3.6 per cent crossed the threshold of 3 per cent, but this was mainly due to the significant increase in capital outlay and loans and advances to power projects (UDAY scheme3). The proposed debt waiver scheme would presumably lead to further deterioration of the fiscal position of the state governments.

Source: State Finances: A Study of Budgets, May 12, 2017, RBI

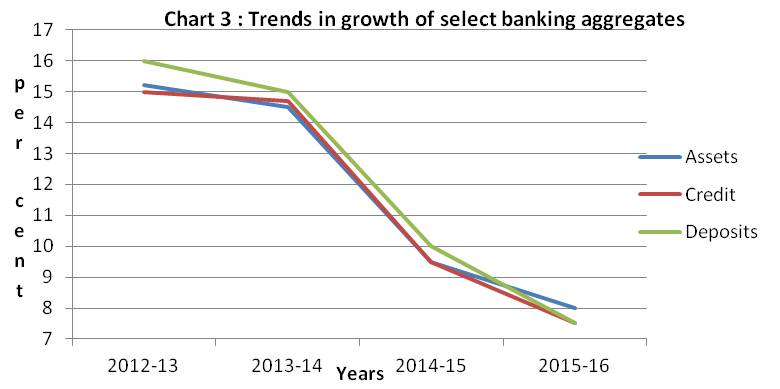

The spate of farm loan waivers also comes at a time when the Indian banking Industry is facing a serious NPA crisis. It appears that at least a sixth of public sector advances are stressed and a significant majority of the assets have turned in to NPAs. For banks under stress, the share of assets under stress has approached or reached 20 per cent. A high and rising proportion of banks’ delinquent loans, particularly those of public sector banks and a consequent increase in provisioning for NPAs has weighed down on credit growth during the past few years reflecting their lower risk appetite and stressed financial position (Chart 3). As of June 2016, the total amount of Gross NPAs for public and private sector banks was around Rs. 6000 billion. Details of 49 banks (Public & Private Sector) is given in Table 6.

These schemes may further vitiate the credit culture and may add to the stressed assets of the banking Industry.

Source: Trend and Progress of Banking in India 2015-16, RBI

| S No. | Bank | Total Advances (Rs. in Billion) | Gross NPA (Rs. in Billion) | Gross NPA (Rs. in Billion) |

|---|---|---|---|---|

| 1 | Allahabad Bank | 1453.28 | 187.69 | 12.92 |

| 2 | Andhra Bank | 1372.28 | 141.37 | 10.3 |

| 3 | Bank of Baroda | 2691.15 | 356.04 | 13.23 |

| 4 | Bank of India | 2743.91 | 439.35 | 16.01 |

| 5 | Bank of Maharashtra | 1031.48 | 130.4 | 12.64 |

| 6 | Bharatiya Mahila Bank Ltd. | 6.27 | 0.03 | 0.4 |

| 7 | Canara Bank | 3116.15 | 304.8 | 9.78 |

| 8 | Central Bank of India | 1857.19 | 251.07 | 13.52 |

| 9 | Corporation Bank | 1427.87 | 157.26 | 11.01 |

| 10 | Dena Bank | 811.14 | 96.36 | 11.88 |

| 11 | IDBI Bank Limited | 2023.04 | 217.24 | 10.74 |

| 12 | Indian Bank | 1221.73 | 86.9 | 7.11 |

| 13 | Indian Overseas Bank | 1492.17 | 302.39 | 20.26 |

| 14 | Oriental Bank of Commerce | 1503.01 | 172.09 | 11.45 |

| 15 | Punjab & Sind Bank | 631.34 | 45.66 | 7.23 |

| 16 | Punjab National Bank | 3569.58 | 550.03 | 15.41 |

| 17 | Syndicate Bank | 1677.59 | 134.75 | 8.03 |

| 18 | UCO Bank | 1151.66 | 214.95 | 18.66 |

| 19 | Union Bank of India | 2429.35 | 255.6 | 10.52 |

| 20 | United Bank of India | 707.81 | 101.04 | 14.28 |

| 21 | Vijaya Bank | 901.99 | 65.89 | 7.31 |

| 22 | State Bank of Bikaner & Jaipur | 740.33 | 45.93 | 6.2 |

| 23 | State Bank of Hyderabad | 1124.2 | 94.36 | 8.39 |

| 24 | State Bank of India | 11933.25 | 931.37 | 7.8 |

| 25 | State Bank of Mysore | 552.28 | 43.23 | 7.83 |

| 26 | State Bank of Patiala | 852.39 | 113.65 | 13.33 |

| 27 | State Bank of Travancore | 682.76 | 64.01 | 9.38 |

| 28 | Catholic Syrian Bank Ltd. | 78.59 | 4.55 | 5.79 |

| 29 | City Union Bank Ltd. | 212.16 | 5.55 | 2.62 |

| 30 | Dhanlaxmi Bank Limited | 67.71 | 4.75 | 7.02 |

| 31 | Federal Bank Ltd. | 594.08 | 17.47 | 2.94 |

| 32 | ING Vysya Bank Ltd. | - | - | - |

| 33 | Jammu & Kashmir Bank Ltd. | 506.4 | 47.15 | 9.31 |

| 34 | Karnataka Bank Ltd | 354.12 | 13.89 | 3.92 |

| 35 | KarurVysya Bank Ltd. | 393.82 | 7.02 | 1.78 |

| 36 | Lakshmi Vilas Bank Ltd. | 201.83 | 4.32 | 2.14 |

| 37 | Nainital Bank Ltd. | 27.76 | 1.45 | 5.21 |

| 38 | Ratnakar Bank Ltd. | 223.73 | 2.53 | 1.13 |

| 39 | South Indian Bank Ltd. | 417.05 | 16.52 | 3.96 |

| 40 | Tamilnad Mercantile Bank Ltd. | 223.29 | 4.89 | 2.19 |

| 41 | Axis Bank Ltd. | 3001.73 | 79.09 | 2.63 |

| 42 | Bandhan Bank Ltd. | 133.58 | 0.29 | 0.22 |

| 43 | DCB Bank Ltd | 134.64 | 2.31 | 1.72 |

| 44 | HDFC Bank Ltd. | 4409.55 | 47.24 | 1.07 |

| 45 | ICICI Bank Ltd. | 3644.29 | 172.08 | 4.72 |

| 46 | IndusInd Bank Ltd. | 936.67 | 8.61 | 0.92 |

| 47 | Kotak Mahindra Bank Ltd. | 1223.84 | 30.59 | 2.5 |

| 48 | Yes Bank Ltd | 1034.11 | 8.45 | 0.82 |

| 49 | IDFC Bank Limited | 497.14 | 30.3 | 6.09 |

Conclusion

Debt Waiver as an initiative appears to be a short-term solution for a long-term malady. The biblical proverb ‘give a man a fish and you feed him for a day, you teach a man to fish, you feed him for life’ is quite apt in this scenario. Major investment in the agricultural sector is the need of the hour which may lead to increased mechanization, improved access to the market place for the farmers, better ware-housing and transportation facilities. This would enhance the profitability of the farmers and would strengthen their capacity to weather rough times such as droughts, natural calamities, which is generally the time when they become susceptible to indebtedness.

From a macro-perspective, debt waivers may also lead to debt burden for the states in terms of borrowing from the market which may eventually push up the yields in the primary market leading to a general hardening of the interest rate scenario in the economy and crowding out of private sector participants. In fact, RBI Governor in the Fourth Bi-monthly Monetary Policy Statement 2017-18 has informed that the combined Central and State Government deficit is in the range of 6 % of GDP and the combined deficit (Centre plus States) may increase by 100 bps in 2017-18. The Governor has further stated that the implementation of farm loan waivers may undermine public spending and may put pressure on prices. This may have adverse impact on the economic stability. RBI has also lowered the growth forecast for the fiscal year to 6.7 % from 7.3 % earlier. Therefore, in the face of slowing down of the economy, farm loan waivers may not prove to be a fiscally sound decision going forward.

References:

1. Essay ‘Sustaining Growth, Ensuring Inclusion’, Rana Hasan.

2. The Constitutional Framework surrounding Debt Relief in India, Aditi Shukla.

3. Report on Task Force of Rural Co-operative Credit Institutions (2006).

4. Report of Expert Group on Agricultural Indebtedness (2007).

5. RBI Annual Report 2016-17.

6. Report on Trend & Progress of Banking 2015-16.

7. Mint Newspaper Article ‘How will farm loan waivers impact the Indian economy’, Aug 10, 2017.

8. India Today ‘Waivers Go A-Begging’, Oct 09, 2017.

9. The Economic Times ‘RBI Warns Govt. against a Loose Fiscal Policy to Drive Growth’, Oct 05, 2017.

End Notes :

1. The author is an AGM in Department of External Investment & Operations, RBI Nagpur. The views expressed by the author in the article are his own and not of RBI.

2. Erstwhile Director, Indira Gandhi Institute of Development Research

3. Ujwal Discom Assurance Yojana (UDAY) was a scheme launched in 2015 by Govt. of India for financial turnaround of Electricity Distribution Companies

(Views expressed are of the author and do not necessarily reflect the views of the VIF)

Image Source: http://www.newsofrajasthan.com

-

The Indian stock market has experienced a remarkable surge in mar

-

On September 2023, JP Morgan announced that it will include India

-

Last month, a leading multinational German investment bank publis

-

E-Commerce globally is on the rise. Relentless innovation in tech

-

The state government of Uttar Pradesh is working diligently to gr

-

The contribution of services sector[1] to the Indian economy is w

-

US President Harry Truman entangled in an array of economic view

-

The year 2022 will go down in history in which the great power ri

Post new comment