Indian Economy is poised to enter a new era of taxation in the form of implementation of much awaited Goods and Services Tax (GST) with effect from July 01, 2017. The GST Bill was passed unanimously in August, 2016 by the Indian Parliament and after ratification by majority of states and upon receiving Presidential assent, it was enacted as Constitution (One hundred and First Amendment) Act, 2016. GST is a herculean initiative by the present Government to rationalise the existing taxation system in the Indian Economy by merging several central and state taxes. The origin of Value Added Tax (VAT)/GST can be traced to the writings of Dr. Wilhelm Von Siemens, famous German Industrialist who proposed the concept in 1918. France was the first country in the World to adopt VAT in 1954. In the Indian context, the journey of GST can be linked to the introduction of VAT in April 2005. The implementation of VAT in turn was based on the recommendations of the Indirect Taxation Inquiry Committee, 1978 chaired by the Former RBI Governor, Shri L.K. Jha. One of the important recommendations of the committee that were made quarter of a century back, was the rationalisation of the existing duty structure on final products and introduction of VAT system in the excise duty.

Overview of India’s Tax System

GST: The Concept

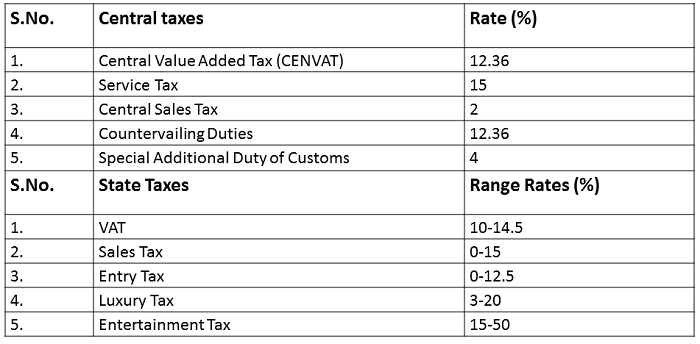

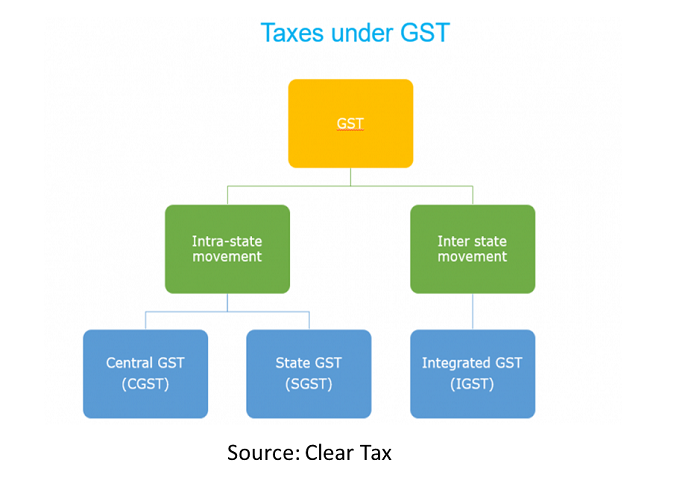

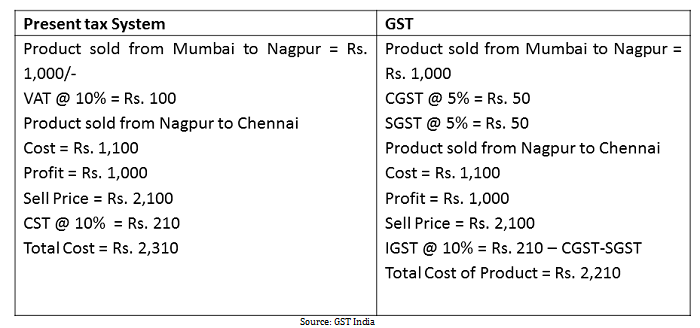

GST is a single unified tax on the supply of goods and services from the manufacturer to the consumer. GST subsumes both Central and State Government taxes. Central taxes subsumed include: Central Excise Duty, Duties of Excise (Medicinal and Toilet Preparation), Additional Excise Duty, Additional Customs Duty and Special Additional Customs Duty. The state level taxes primarily include: State Value Added Tax, Entertainment Tax, Central Sales Tax, Octroi & Entry Tax, Purchase Tax, Luxury Tax, etc. GST is different from the earlier avatar of ‘VAT’, since VAT is imposed at different stages of production whereas GST is levied at national level on the consumption of goods and services. The novelty of GST is that the ultimate consumer will have to bear GST charged by the last dealer in the supply chain, the credits of input taxes paid at each stage will be available in subsequent stages. According to Adam Smith, the renowned economist of the 19th Century, a good taxation system must satisfy the cannon of convenience and economy. GST gets full marks on this account since on account of being a single tax, it would be convenient for the tax payers. On account of setting up of a user friendly IT system in the form of Goods and Service Tax Network (GSTN) portal it will also be easier to administer. GSTN is a non-profit organization with 49 percent Government of India and 51 percent share by Financial Institutions. Unlike the current indirect tax where there are multiple sites, GSTN is poised to provide easier and user friendly access to tax payers and Government to track the status of returns and payment.

Select Cross-Country Experience

Malaysia, an Asian peer of India, introduced GST in April, 2015. The primary objective behind implementation of GST was to widen the tax base since only 10 percent Malaysians were paying income tax; and with the fall in global oil prices, Malays ian Government was prompted to look towards alternative sources of revenue. A major hurdle faced in the implementation process was the exemption of many essential products from GST even though at six percent, Malaysia’s GST rate is one of the lowest in the World. However, it has been observed subsequently that on account of introduction of GST, the cost of doing business in Malaysia has come down since the tax burden has been shifted from manufacturers to consumers. On account of implementation of GST, the indirect tax collection has been forecasted to increase by 5.5 percent to MR 56.6 billion, the number of claimants has increased to 4,23,920 as of September, 2016.

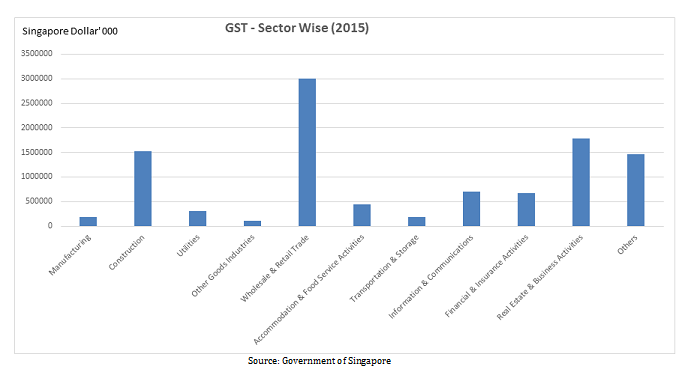

Malaysia’s neighbor, Singapore introduced GST way back in 1994 at three percent which now stands at seven percent from July, 2007. As per the norms, GST is levied on goods and services supplied in Singapore by any taxable person in the course of business and goods imported in to Singapore by any person. In 2007, in order to alleviate the impact of tax increase, the tax increase was accompanied by an off-set package. The off-set package consisted of direct transfer benefits in the form of cash pay-outs and rebates. The primary motive apart from widening the tax base, was to make the tax base more resilient in view of ageing population and work force. The major contribution to GST revenue collection in 2015 was Wholesale and Retail Trade (29 percent).

GST was introduced in Canada in 1991. It replaced the Manufacturer’s Sales Tax (MST) (13.5 percent). The reason for replacement of MST by GST was to promote the manufacturing sector’s ability to export competitively. GST is levied on supplies of goods or services purchased in Canada except on essential items such as groceries, residential rent, medical services and financial services. Businesses that purchased goods and services that are consumed, used or supplied in the course of their “commercial activities” can claim “input tax credits”. In July, 2006, the Canadian Government had reduced the tax by one to six percent. However, some of the Canadian provinces impose their own sales tax which distorts prices in the economy.

Implementation

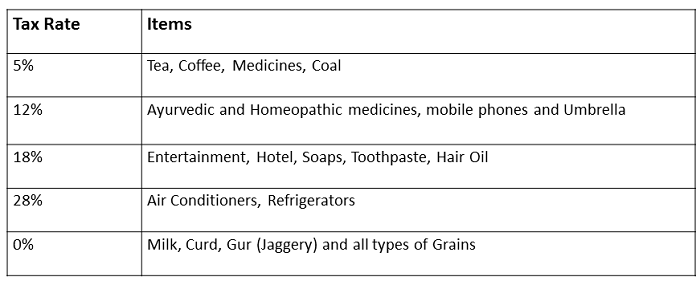

Union Cabinet in compliance with Article 279 (A) of the Indian Constitution constituted the GST Council and GST Council Secretariat. The GST Council is chaired by the Union Finance Minister, Union Minister incharge of Revenue, Minister in charge of taxation, or any one Minister nominated by each state government. State government representatives enjoy two-third vote share, and remaining one third belongs to the Central Government. The mandate of GST Council is to recommend the goods and services that are to be subjected or exempted from the GST and GST rates. The 14th Meeting of the GST Council was held over a two-day period (May 18-19, 2017) in Srinagar and GST rates for 1,211 items were recommended. A five slab GST rate system has been recommended – zero percent, five percent, 12 percent, 18 percent and 28 percent. Essential commodities such as Milk, Curd, Gur (jaggery) and all types of grains would attract zero percent GST rate, whereas luxury goods such as air-conditioners and refrigerators would attract the highest GST rate of 28 percent.

Similarly, services have been distributed under five GST slabs – zero percent, five percent, 12 percent, 18 percent and 28 percent. Zero tax would be levied on travelling in Metro rail and local train and pilgrimages. Whereas the highest tax slab of 28 percent would be levied on dining in luxury restaurants and staying in hotels. The biggest take away from the deliberations of the GST Council was reachinga consensus on clubbing the bulk of items in to two standard rates of 12 and 18 percent. Notably the two standard rates of 12 and 18 percent account for 60 percent of all items, and only 19 percent of the items have been pushed in to higher rate of 28 percent. Another significant step has been the rationalisation of a list of exemptions. The low GST rate on items of daily use are a vindication of the Government’s commitment of establishing a new tax regime which will be non-inflationary.

The 15th GST Council meeting was held on June 03, 2017, the GST Council in the meeting has cleared all the pending rules related to transition provisions and returns, all the states have agreed to GST roll-out from July 01, 2017 (except seven states). It has been decided that gold, gems and jewellery will be taxed at three percent and apparel costing below Rs. 1,000 will be taxed at five percent. An important development in the meeting has been setting up of a committee with reference to complaints regarding anti-profiteering clause. It has also been decided to constitute three tier structure of ‘project management’ of GST with Revenue Secretary as the head of the structure, followed by a Project Management which will be called ‘GST Implementation Committee’ and eight standing committees. In addition there will be 18 sectorial groups to look in to specific issues of sectors such as telecom, banking, mining and pharmaceuticals.

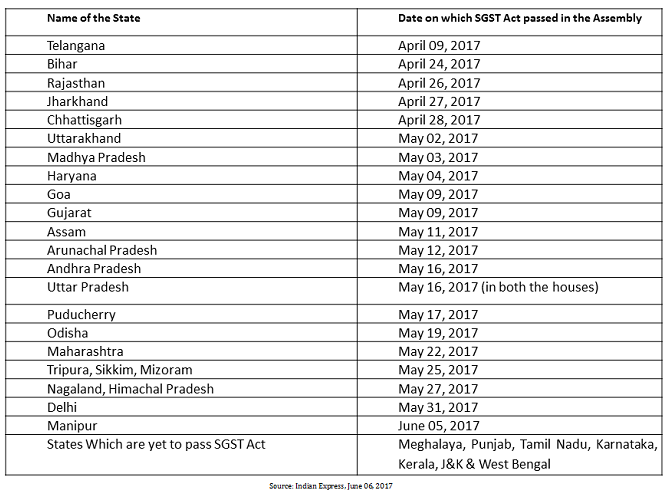

Passage of SGST Act

Impact on Inflation

Alan A Tait, on behalf of the International Monetary Fund (IMF), had conducted a survey in 1990. It was found that in case of 22 countries, on account of implementation of VAT, no major impact on Consumer Price Index (CPI) was identified. In case of another eight countries, it was identified that the introduction of VAT was associated with a highly defined ‘once-and-for-all’ shift in consumer price index. In seven other cases although the shift was permanent, there was no acceleration in the rate of change in prices attributable to VAT. Therefore, cross-country experience points towards primarily non-inflationary impact of VAT. In the Indian context, on account of essential commodities either attracting nil or lower GST rate, it is perceived that the implementation of GST would not stroke inflationary fires in the economy. In fact as per the Revenue Secretary, Government of India, if the reduction of taxes is passed on to the consumers by the end of the financial year, the CPI is expected to come down by two percent.

Macro-Economic Implications

The macro-economic implications of the implementation of GST are enumerated as under:

i. The implementation of GST would give further impetus to the services sector since the services sector contribute 54 percent of India’s Gross Value Added at current prices (Rs. 73.79 lakh crore in 2016-17).

ii. The implementation of GST would lead to reduction of compliance cost on account of setting up of user friendly IT system in the form of GSTN.

iii. As per the fiscal road map laid out, fiscal deficit is targeted at 3.2 percent of GDP in 2017-18 and at three percent in 2018-19. Post implementation, the gross fiscal deficit is expected to decline by 0.7-1.2 percent of GDP.

iv. As per the International Finance Discussion Note titled “The Effect of the GST on Indian Growth”, authored by Eva Van Leemput and Ellen A. Wiencek, Board of Governors of the Federal Reserve System, the implementation of GST would lead to real GDP gains of 4.2 percent.

v. S&P Global Ratings had kept India’s sovereign rating unchanged at lowest investment grade (BBB-) and had ruled out an upgrade till 2017 end. One of the concerns of S&P was the weak public finances. It can be inferred that the adoption of GST would strengthen public finance since it would lead to improved efficiency in tax collection.

References

1. RBI Study (2017), “Goods and Services Tax: A Game Changer”, State Finances: A Study of Budgets of 2016-17.

2. Report of the Indirect Taxation Enquiry Committee, 1978 (Chairman: LK Jha).

3. Website of Goods and Services Tax Network (www.GSTN.org).

4. Website of Ministry of Finance, Singapore (www.mof.gov.sg).

5. Editorial column ‘THE LAST LAP’ of Indian Express dated May 20, 2017.

6. Alan A Tait(1991), “Value-Added Tax: Administrative & Policy Issues”, IMF Occasional Papers.

7. Website of Ministry of Statistics &Programme Implementation (www.mospi.nic.in).

8. Eva Van Leemput and Ellen A. Wiencek (2017), “The Effect of the GST on Indian Growth”, International Finance Discussion Note, Board of Governors of the Federal Reserve System.

9. Live Mint (2016), “S&P’s credit rating for India unchanged, outlook stable”.

(The Author is an Assistant General Manager in Department of External Investment & Operations, Reserve Bank of India (RBI), Nagpur.)

(Views expressed are of the author and do not necessarily reflect the views of the VIF)

Image Source: http://techstory.in

-

India possibly can boast of having one of the largest (nearly 35

-

Following the visit of an Indian delegation to Afghanistan in Mar

-

The plenary sessions of the Chinese People’s Political Consulta

-

Background Chief of Army Staff (COAS) of the Indian Army, Gene

-

Premise This work attempts to analyse the following premise:-

-

Modi is the first and only Prime Minister to place before the peo

-

From being an intensely hated person, he has become the most admi

-

The Jallianwala Bagh massacre on April 13, 1919, in Amritsar, Pun

Post new comment